Investment Philosophy

The Yale Investment Office seeks to provide high inflation-adjusted returns to support current and future needs of the University. We work to establish an appropriate risk-adjusted asset allocation and seek out long-term partnerships across the globe with managers who provide deep analytical insights and improve the operations of public and private businesses. Over the past 30 years, relative to the median endowment, Yale’s asset allocation has contributed 1.9% per annum of outperformance and Yale’s superior manager selection contributed an additional 2.4% per annum.

Yale's portfolio is structured using a combination of academic theory and informed market judgment. The theoretical framework relies on mean-variance analysis, an approach developed by Nobel laureates James Tobin and Harry Markowitz, both of whom conducted work on this important portfolio management tool at Yale’s Cowles Foundation. Because investment management involves as much art as science, qualitative considerations play an extremely important role in portfolio decisions. The definition of an asset class is quite subjective, requiring precise distinctions where none exist. Returns and correlations are difficult to forecast. Historical data provide a guide, but must be modified to recognize structural changes and compensate for anomalous periods. Quantitative measures have difficulty incorporating factors such as market liquidity or the influence of significant, low-probability events. In spite of the operational challenges, the rigor required in conducting mean-variance analysis brings an important element of discipline to the asset allocation process.

David F. Swensen '80 Ph.D., '14 L.H.D.

Investor and Teacher Portrait: Alastair C Adams PPRP, April 1, 2015

Asset Allocation

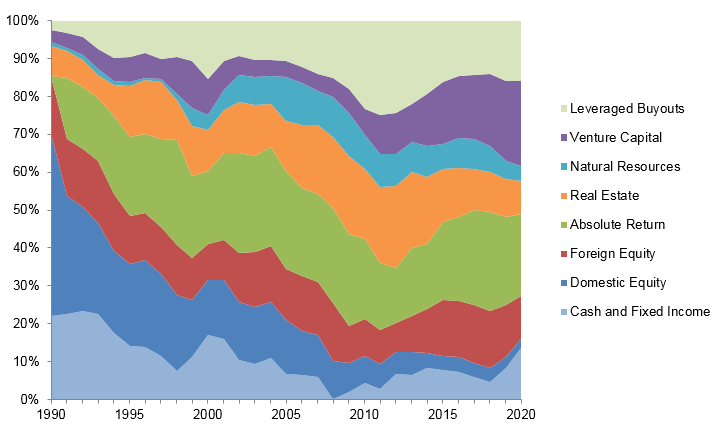

Over the past 30 years, Yale dramatically reduced the Endowment's dependence on domestic marketable securities by reallocating assets to nontraditional asset classes. In 1989, nearly three quarters of the Endowment was committed to U.S. stocks, bonds, and cash. Today, domestic marketable securities account for less than one-tenth of the portfolio, while foreign equity, private equity, absolute return strategies, and real assets represent over nine-tenths of the Endowment.

The heavy allocation to non-traditional asset classes stems from their return potential and diversifying power. Today's actual and target portfolios have significantly higher expected returns and lower volatility than the 1985 portfolio. Alternative assets, by their very nature, tend to be less efficiently priced than traditional marketable securities, providing an opportunity to exploit market inefficiencies through active management. The Endowment's long time horizon is well suited to exploiting illiquid, less efficient markets such as venture capital, leveraged buyouts, oil and gas, timber, and real estate.

Supporting the University

The Endowment spending policy, which allocates Endowment earnings to operations, balances the competing objectives of (1) supporting today’s scholars with annual spending distributions and (2) maintaining that support for generations to come. The spending policy manages the trade-off between these two objectives by using a long-term spending rate target combined with a smoothing rule, which adjusts spending in any given year gradually in response to changes in Endowment market value.

Using the metrics of stable operating budget support and purchasing power preservation, simulations of Endowment performance demonstrated substantial improvement over the past thirty years. As Yale improved diversification by allocating more of the Endowment to the alternative asset classes of absolute return, private equity, and real assets, risks plummeted for both spending volatility and purchasing power degradation.

In 1985, when alternative asset classes accounted for only 11 percent of the Endowment, Yale faced a 10 percent chance of a disruptive spending drop, in which real spending drops by 10 percent over two years, and the average spending drop in the worst ten percent of simulations was 20 percent. Furthermore, the 1985 portfolio faced a 21 percent chance of purchasing power impairment, in which real Endowment values fall by 50 percent over fifty years. By 2019, when absolute return, private equity, and real assets accounted for approximately 77 percent of the Endowment, disruptive spending drop risk fell to 5 percent, the average worst spending drop decreased to 12 percent, and purchasing power impairment risk declined to 2 percent.